Update after Q3 2023 Earnings Season

I know I am late but let’s have a look at how the companies I’ve written about performed in Q3 2023.

AMG Critical Materials N.V.

Performance -39.16%

The combo of underwhelming results and a lowered guidance for 2023 and 2024 sunk the stock AMG after earnings driven by the global decline in metal prices, mainly lithium and ferrovanadium.

Q3 2023 Results

Revenue $369M (-13% vs Q3 2022).

EBITDA $54M (-48%).

Cash from Operating Activities $25M (-67%).

EBIT $40M (-56%).

Diluted EPS $0.00 (vs 2.09).

ROCE 28.4% (vs 29.5%).

Guidance

2023 EBITDA guidance lowered to $320M from an already lowered guidance range of $350M-$380M (original EBITDA guidance for the year was at least $400M).

2024 EBITDA guidance $200M with a stronger performance in the second half of the year (not factoring in the Lithium Hydroxide refinery in Germany which is scheduled to start up in Q2/Q3 2024).

Conference Call

New Corporate structure from January 1 2024 - as it happened with AMG Lithium in 2023, management has decided to create two more corporate entities, AMG Vanadium and AMG Technologies, each with its own leadership team and operating management.

For the first time in the history of AMG, divestments are on the table - CEO Heinz Schimmelbusch announced that there will be several divestments to streamline the portfolio. AMG Technologies division is the more likely one to be affected, but I wouldn’t rule out the sale of AMG Vanadium.

AMG Engineering signed $81M in new orders during the quarter, 51% higher than in Q3 2022 - the order backlog is also at record highs ($341M) thanks to the strong growth period in the aerospace market.

Mibra Mine Spodume expansion project is behind schedule due to delivery delays of electronic components for porcessing automation - the plant shutdown to complete the expansion from 90,000 tons to 130,000 tons will now take place in Q1 2024. Full run rate capacity is expected to be achieved in Q3 2024.

The first module of the battery-grade Lithium Hydroxide refinery in Bitterfeld (Germany) is in the initial phases of comissioning - the ramp-up and the qualification process is planned for Q2/Q3 2024. Production is expected to reach 7,000 tons in 2024 (not included in EBITDA guidance); in 2025 management expects to produce and sell the full capacity of the module (20,000 tons).

The Lithium project in Portugal with Grupo Lagoa will begin basic engineering in December 2023 - according to current data, the plan is to build a 150,000 ton lithium concentrate plant at the site. This resource will provide sufficient feedstock for an additional module in Bitterfeld.

The new Vanadium spent catalyst roasting facility in Zanesville (Ohio) operated at full capaticity in Q3 - the plant was affected by a defective fan in Q2.

The Vanadium electrolyte plant at AMG Titanium in Nuremberg is under construction - the capacity of the plant will be 6,000 cubic meters; production is expected to start in Q1 2024.

The Phase I of the Supercenter project with Shell in Saudi Arabia is expected to reach FEL3 status by the end of the year.

The Mibra mine in Brazil delivered 16,000 tons of lithium concentrate in Q3 - the average realized sales price was $2,395 per ton CIF China and the average cost per ton CIF China was $529.

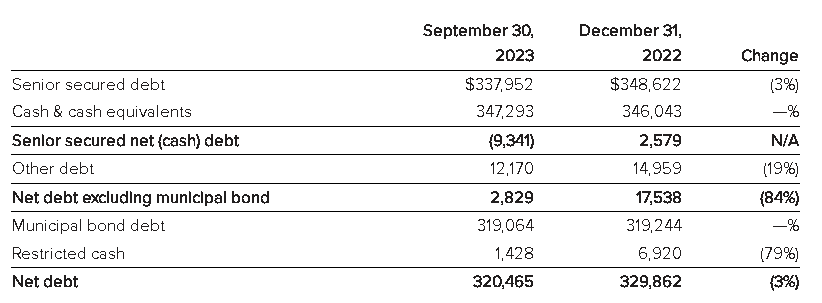

Management is not worried about the upcoming increase in debt to finance the expansion projects - the key covenant is 3.5x net senior secured debt to EBITDA, so it excludes the municipal bond which is currently the main financing instrument of the company.

CAPEX for 2024 will be in the $175M to $200M range.

Share buybacks are not considered at the moment - although the valuation of the company is very low right now, the capital allocation policy of AMG is focused on growth.

A decision for a second module on the refinery plant in Bitterfeld will me made at the end of 2024 or beginning of 2025.

News

CEO Heinz Schimmelbusch bough 45,536 shares at an average price of €20.54 the 9th of November.

The opening of the refinery in Bitterfeld grabbed some atenttion from the german press (Mitteldeutsche Zeitung) and even The Guardian.

Analysis

Not many good news for AMG last quarter: lithium prices sank affecting the results and the guidance of the company. Moreover, the delay on some key expansion projects didn’t help either. As such the stock price plummeted from almost €50 per share to less than €20. I managed to buy some shares in the 17€ area to lower my average purchase price to €22.66. The investment thesis still stands, lithium prices will go up and down but the key is to complete the expansion projects (specially the refinery in Germany) to intagrate the whole supply chain.

Construcciones y Auxilar de Ferrocarriles S.A.

Performance +19.55%

Solid results from CAF: this time the usual revenue growth was accompanied by a much needed improvement in profitability. The bus division Solaris keeps winning new contracts at a fast pace and is now the market leader in Europe.

9M 2023 Results

Revenue €2,735M (+25% vs 9M 2022).

Order Intake €2,707M (-29%).

Backlog €13,222M (-0%).

EBIT €128M (+32%).

EBIT Margin 4.7% (vs 4.4%).

News

CAF selected by London North Eastern Railway to supply first tri-mode intercity fleet - the project includes also the maintenance services for 8 years. Value of the contract exceeds €500M.

Analysis

As if have stated over and over, my investment thesis about CAF was centered in two cornerstones: first of all, the greenization of public transport which will translate into revenue growth and secondly the improvement in profitability at all levels after the supply chain and inflation issues suffered in the last couple of years. For the first time in a while the profitability part of the equation is showing signs of life, which should continue in the upcoming quarters at a steady pace.

Chargeurs S.A.

Performance -21.58%.

The takeover bid launched last Thursday by CEO Michaël Fribourg at 12€ per share taking advantage of the low stock price has taken centre stage right now when talking about Chargeurs. Q3 results were mostly in line with previous quaters and with analaysts’ expectations.

Q3 2023 Results

Total Revenue €150.8M (-13.8% vs Q3 2022, -7.6% like-for-like).

Chargeurs Advanced Materials €64.1M (-16.5%, -13.9% LFL) - positive signs of recovery so the worst seems to be over now for CAM: five consecutive months of monthly new orders above 2022 and the montly sales volumes in September and October 2023 have been above 2022 levels. The decline in revenue is easing compared to H1 2023 which had a very tough comparison base due to a strong restocking from customers in H1 2022 after COVID.

Chargeurs PCC Fashion Technologies €48.6M (-13.1%, +4.7% LFL) - as in previous quarters, a resilient performance compared to a strong 2022. The slowdown in sales in Europe (particularly to luxury brands) was compensated thanks to the good momentum in Asia. The expansion across all apparel segments could bring an increase in its market share in the coming months.

Chargeurs Museum Studio €22.8M (+11.8%, +13.6% LFL) - the growth engine of the group, CMS keeps delivering quarter after quarter.

Chargeurs Luxury Fibers €13.2M (-39.4%, -36.5% LFL) - sharp decline in revenues due to a fall in wool prices and a high level of conventional wool invetories held by spinners and weavers. Sales of Nativa certified wool now account for more than 20% of sales volumes vs 10% in 2022.

Chargeurs Personal Goods €2.1M (consolidated in December 2022) - Chargeurs is focus in developing Cambridge Satchel (new logo, opening of first permanent shop in London and new online site) and Altesse Studio (products now available in Galleries Lafayette in France and it has entered the American market with a physical sales outlet in New York). Swaine is not consolidated yet.

Guidance

2024 guidance reitarated - Revenue above €800M, EBITDA margin between 9% and 10% and a debt/EBITDA multiple of less than 3x.

Chargeurs Museum Studio revenue guidance confirmed - €120M for 2023 and €150M for 2024.

News

Chargeurs PCC opens a new innovation studio in Porto (Portugal).

Stella McCartney spotlights wool partner Nativa at Paris Fasion Week.

Nativa and ba&sh partner on regenarative agriculture programme in Uruguay.

Chargeurs Museum Studio keeps growing - Opening of Chargeurs Museum Studio in France and appointment of Catherine Castillon as new Managing director of Skira Editore. Also, Skira Editore has designed and produced the exhibition Humanity by British photographer Jimmy Nelson in Milan (Italy).

Chargeurs tried to acquire the luxury house Baccarat last summer - the prestigious crystalmaker Baccarat is for sale after its former chinese owner defaulted in 2020. The creditors’ price expectations (€400M) were too high for Chargeurs, which is still looking for an acquisition in the Quiet Luxury area.

Analysis

Results not that much different from previous quarters: CAM is still weak but improving slowly while the bright spot is Museum Studio. The analysis of the results is now a bit outdated given the urgency of the takeover bid. I will post a new article later in the week expressing my thoughts about the offer.