Update after FY 2022 Earnings Season

Now that earnings season is over let’s have a look at the companies I have presented in the last months.

AMG Advanced Metallurgical Group N.V.

Great results from AMG in 2022, where EBITDA, revenue, gross profit, operating cash flows, return on capital employed, and net income were the highest in the company’s history. This historical result was achieved thanks to its Clean Energy Materials division, more specifically to AMG Lithium.

2022 FY Results

Revenue $1,642M vs $1,680M consensus vs $1,204M 2021 (+36%).

EBITDA $343M vs €137M 2021 (+150%).

AMG Lithium EBITDA $215M, 63% of the group total.

2022 Q4 EBITDA $104.0M vs $98.8M consensus.

Adjusted EPS $5.73 ($5.87 unadjusted) vs $5.35 consensus.

2022 Dividend raised to 0.70€ from 0.60€ (including the interim dividend 0.30€ paid in August 2022).

2023 Guidance

Reaffirms EBITDA guidance of at least $400M in 2023.

2023 CAPEX $175M to $200M, mainly from the Lithium mine expansion in Brazil and the construction of the lithium hydroxide plant in Germany.

Conference Call

During the conference call management sent some interesting messages for the future of AMG:

Management is very confident in achieving its 2023 EBITDA guidance of at least $400M - when asked by an analyst if the recent drop in lithium prices would jeopardize its outlook for 2023, CEO Heinz Schimmelbusch stated that its assumptions of lithium prices are below current market prices and quite conservative so there’s no need to change the guidance.

The expansion project at the Lithium mine in Brazil progresses at good pace - there will be a shutdown for a few weeks at the end of Q2 to switch production from 90,000 tons to 130,000 tons.

After AMG Lithium, two more subsidiaries will be formed with its own board and management team: AMG Vanadium and AMG Technologies - announcement expected to be made at the next Annual General Meeting.

The door is open to sell any of its businesses if the right offer arrives - management hinted that some of its businesses in the Critical Materials division (less than 10% of total EBITDA) could be sold soon.

AMG Vanadium expansion project completed in Q4 2022 in Ohio will reach full production levels in Q2 2023.

First module of the Lithium hydroxide refinery in Germany expected commissioning in Q4 2023, 6 months more to reach full production.

News

AMG Lithium signs MOU with FRYER Battery for supply of battery-grade Lithium Hydroxide - with this new MOU the first module of the hydroxide refinery in Germany is fully booked, additional modules could be built if the demand is strong.

AMG sells its first commercial LIVA battery to Wipotec - no information about the price paid but it’s a good first step for the development of the LIVA battery.

AMG announces approval for Vanadium electrolite plant at AMG Titanium - the capacity of the plant is 6,000 cubic meters of vanadium electrolyte and production is expected to start at the end of 2023. CAPEX expected to be $15M.

AMG announces Tantalum strategic partnership with Nippon Mining & Metals Corporation - JXNMM will invest in the expansion of tantalum concentrate production that is occurring in combination with the expansion of spodumene capacity. All tantalum pre-concentrate will be processed at Mibra Mine and subsequently sold to TANIOBIS.

Key Dates

March 30th - Capital Markets Day, mainly focused on Lithium.

May 3rd - Q1 2023 Results.

May 4th - Annual General Meeting.

Analysis

As expected, I think the results have been quite strong, and they should keep improving in the coming quarters (unless lithium prices crash). A potential sale of the non-strategic businesses (AMG Technologies and any of the Critical Materials Division businesses) would be great news becasuse AMG would get a cash inflow to finance the expansion projects in AMG Lithium and AMG Vanadium. So far the investment thesis holds, as the expansion projects kick off the performance should keep improving and eventually the stock price will follow.

Construcciones y Auxiliar de Ferrocarriles S.A.

As expected, CAF’s results have been greatly impacted by inflation and supply chain constraints: despite revenue growing strongly from 2021, profitability has greatly worsened. The outlook for 2023 is more optimistic, marking the beginning on the recovery in profitability.

2022 FY Results

Revenue €3,165M (+8% vs 2021)

Strong order intake at €6,205M (+64% vs 2021) and backlog at €13,250M (+37%)

EBITDA margin 7.3% (-1.4pp vs 2021)

EBIT €139M vs €165M 2021

EBIT margin 4.4% (-1.2pp vs 2021)

EPS €1.52 vs €2.51€ 2021

2022 Dividend lowered to €0.86 from €1.00

2023 Guidance

2023 Revenue >€3,400M (+10-15%).

Improved profitability vs 2022.

Confirms the goals of the 2026 Strategic Plan - Revenue of €4,800M and EBIT of €300M.

Conference Call

CAF does not hold a conference call after presenting results.

News

No significant news in the last months but a bunch of tender offers won to supply green buses under the Solaris brand:

Solaris will deliver 100 Urbino full hybrid buses to Cagliari (Italy).

CAF is the Main Candidate to win the €330M contract to renew ATM Milano’s bus fleet.

Key Dates

May 5th - Q1 2023 Results

June 10th - Annual General Meeting

Analysis

After a weak 2022, margins must improve in 2023. There’s no doubt that the growth in revenues will keep at a nice pace, but for CAF the key is profitability. The outlook for management looks better for 2023, so let’s see how the next quarters develop.

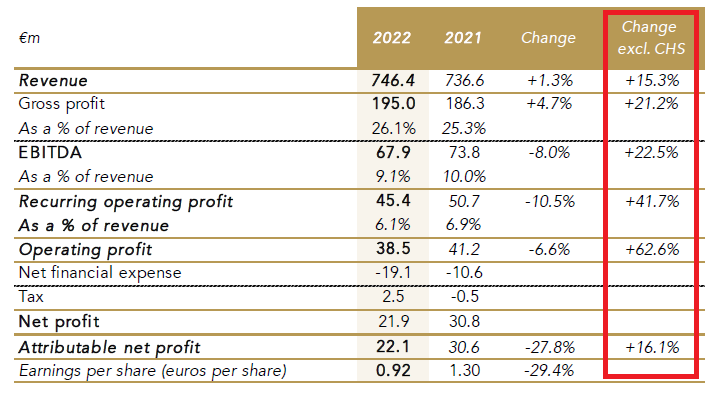

Chargeurs SA

Strong performance from Chargeurs compared to a very atypical 2021, where the results were heavily impacted by the stellar performance of Chargeurs Healthcare Solutions thanks to the sales of PPE during the COVID pandemic. At first look it may look like a weaker year than 2021, but excluding CHS we can assess that the results have been remarkable.

Results

2022 Dividend lowered to 0.76€ from €1.24 in 2021 (including an interim dividend of €0.22 paid back in October 2022) - The dividend can be received in cash or in shares.

Net Debt 2022 €174.7M (2.6x Net Debt/EBITDA ratio) vs 2021 €109.3M (1.5x Net Debt/EBITDA) - Mainly due to an increase in Working Capital Requirements in Chargeurs Advanced Materials.

Performance by Business

Chargeurs has made another rearrangement in its business lines, creating Chargeurs Personal Goods inside the Luxury Division to group the B2C brands that operate in the luxury personal goods segment (Swaine, Altesse Studio and The Cambridge Satchel Company). As a consequence, Chargeurs Personal Care has been eliminated and now the protection mask business is reported in Chargeurs Healthcare Solutions inside the Technologies Division. In the future, as the health environment normalizes, CHS’s financial statements will be consolidated within Chargeurs PCC Fashion Technologies.

Technologies Division

1 - Chargeurs Advanced Materials - Revenue €332.6M (-2.4% vs 2021, -6.3% LFL), EBITDA margin 9.6% (vs 10.8% 2021), EBIT margin 6.9% (vs 7.7% 2021).

2 - Chargeurs PCC Fashion Technologies - Rev €220M (+33.4%, +32.4% LFL), EBITDA mg 11.0% (vs 7.4%), EBIT mg 7.7% (vs 2.9%).

3 - Chargeurs Healthcare Solutions - Rev €6.4M (-93.2%, same LFL), EBITDA mg 81.3% (vs 23.8%), EBIT mg 67.2% (vs 22.9%).

Luxury Division

1 - Chargeurs Museum Solutions - Rev €87.2M (+75.1%, +34.5% LFL), EBITDA mg 9.5% (vs 14.5%), EBIT mg 6.0% (vs 9.4%)

2 - Chargeurs Luxury Fibers - Rev €94.7M (+9.9%, +7.9 LFL), EBITDA mg 2.2% (vs 1.4%), EBIT mg 2.1% (vs 1.2%).

3 - Chargeurs Personal Goods - Rev €5.5M, EBITDA mg 10.9%, EBIT mg 5.5%. Newly created business line so these numbers only reflect the performance in Q4 2022.

2023 Guidance

Chargeurs doesn’t give a guidance for the year but gives us some hints about how 2023 might develop.

Gradual normalization expected through the year, with a stronger second half of the year.

Order book for Chargeurs PCC Fashion Technologies remains at high level.

Prospects of a recovery in Chargeurs Advanced Materials.

Revenue of at least €120M for Chargeurs Museum Studio.

Expected growth in Chargeurs Personal Goods.

Potential key acquisiton within the Luxury Division.

Reaffirms 2025 targets - €1B in revenue and €100M in EBIT excluding acquisitions.

Conference Call

Really interesting earnings call where management got deep about the performance and future of Chargeurs.

CAPEX for 2023 will not be higher than 2022, which was around €10.5M.

Chargeurs Advanced Materials is bouncing back to normal levels after a weak Q4 2022. - Management explained that last autumn customers started cancelling or reducing orders mainly in Europe due to high energy prices. Now activity is picking up and should be back at normal levels at the end of Q2 2023. These reduction in orders have cost Chargeurs around €8M-€10M in EBIT and €20M-€30M in Working Capital Requirements.

Continuing with CAM, they have raised prices in 2022 by 15% - with normal volumes CAM would have reached a 10% EBIT margin.

Prince increase of 7% in 2022 in Chargeurs PCC Fashion Technologies.

Management reaffirmed Chargeurs Museum Solutions EBIT margin between 15-20% for the long term - The performance should keep improving each year due to three reasons: firstly, the early years of a museum project have lower margin; secondly, improvement in the UK and the Netherlands after COVID; lastly, revenues will raise by crosselling between businesses (for example recently acquired Skira Editore attained its best month ever in January 2023 thanks to the opportunities that opened up for them after joining Chargeurs).

CMS EBIT in 2023 could double vs 2022.

CMS geographical distribution - 50% US, 1/3 Middle East and Asia, rest Europe

Backlog of €200M in CMS.

There are identified targets for the key acquisition in the luxury division - Analysts worried about the high multiples paid nowadays for luxury companies and where the debt levels might get after the acquisition. CEO Michaël Fribourg sounded quite confident, stating that nowadays is more of a “buyers market” than a “sellers market” and that they have demonstrated in the last years that they have a successful process to select the right company to acquire.

Chargeurs has accumulated 900,000 treasury shares, almost 4% of the company, taking advantage of lower prices - 80% of them will be cancelled and the rest will be for compensation purposes.

News

No remarkable news in the last month.

Key Dates

April 26th - Annual General Meeting.

May 2nd - Ex-dividend date.

May 23rd - Q1 2023 Results.

Analysis

The results have been remarkable in a high inflation environment, thanks to a large extent by the stellar performance in Chargeurs PCC Fashion Technologies. In 2023 there’s room for improvement in Chargeurs Advanced Materials and Chargeurs Museum Solutions, with management outlook pointing in that direction. Waiting for a key adquisition in the Luxury Division that could completely transform Chargeurs, the company strategy of premiutization and adquisitions continue to perform well.