Obrascón Huarte Laín S.A.

A deep value turnaround hiding in the global infrastructure boom.

Summary

Obrascón Huarte Laín S.A. (OHLA) is a Spanish construction and civil engineering company, mainly involved in infrastructure and commercial property construction and the operation of concessions.

Burdened by high debt in recent years, a recent debt restructuring and capital raise have improved its balance sheet health.

Other roadblocks in the form of court challenges are also clearing up offering a clear path ahead.

Ambitious 2029 Strategic Plan progressing at a strong pace, already delivering tangible improvements in profitability.

Trophy asset in the center of Madrid could wipe out the entirety of its (very costly) debt.

Trading at a severe discount relative ot its peer group, the stock offers a highly conservative path to double from current levels.

Introduction

Global infrastructure is undergoing its most massive investment wave in modern history. Driven by the critical need to overhaul aging Western infrastructure, build a new AI infrastructure ecosystem and a sustain a green energy revolution, trillions of euros are flooding the sector. As a result, many European construction companies have multiplied their valuation in the past few years.

But there are still highly asymmetric turnarounds hiding at the very bottom of the valuation ladder. Enter OHLA (BME:OHLA). Completely overlooked by the market due to a decade of poor legacy performance, current management has completely turned around the company at the operating level.

Furthermore, the company holds non-core assets primed for monetization that could completely clear its corporate debt, legal disputes are closing after a decade, margins are expanding and revenue is expected to grow strongly mainly thanks to its strong presence in the US. And it’s trading at a fraction of its peers.

Could OHLA be the next european construction company to skyrocket?

Dissecting OHLA

OHL was founded in 1999 with the merger of the historic firms Obrascón-Huarte (which had merged themselves one year before) and Construcciones Laín under the direction of Juan Miguel Villar-Mir. During the following decade OHL achieved impressive growth, taking advantage of the construction and infrastructure boom in Spain.

As we know good times usually don’t last forever. The company decided to aggressively expand internationally after the 2008 financial crisis to avoid the Spanish property crash; it worked at first, with the stock bouncing back near all-time highs in 2014, but the growth was built on debt (reached €4.0B in 2014). The early termination of some legacy projects in Canada and Qatar and a bribery scandal in Mexico put a lot of financial pressure on the company, which was forced to book a €520m provision in 2016. At that time, the stock had already lost more than 90% off its 2014 peak and rating agencies downgraded OHL’s debt deep into junk status.

On May 2020, the Mexican Amodio brothers (Luis and Mauricio) stepped in to replace the Villar Mir family as the largest reference shareholder acquiring their 16% stake on the company for €50.4m (€1.10 per share at the time). The year after, following a capital increase and a deep debt restructuring to stabilize the company’s financial structure, the Amodio family reinforced their commitment growing their stake to almost 26%.

This move solidified their absolut operational control, rebranding the company as OHLA to include their initial on the name and making a much needed change in the strategy of the company, which was on the brink of collapse.

Nowadays, OHLA has five main divisions:

Construction (€3.303B Revenue, 82.14% of total Revenue)

The main division of the company, it accounts for almost 80% of its revenue. The Construction division engages in all manener of civil engineering and building construction works for public and private customers (mainly in Spain, USA, Chile and the Czech Republic) including roads, hospitals, ports, mining, airports, railroads, etc.

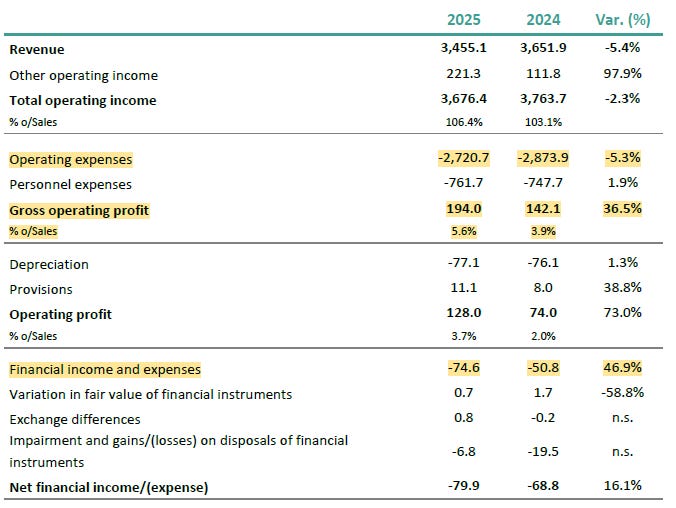

Sales of the division in 2025 decreased very slightly to €3.303B from €3.327B in 2024, but EBITDA almost doubled to €232.8m (from €157.9m in 2024), thanks to an improvement in the EBITDA margin to 7.0% from 4.7% the previous year. This EBITDA margin is on par, or even better, with larger european construction companies which are trading at much higher multiples.

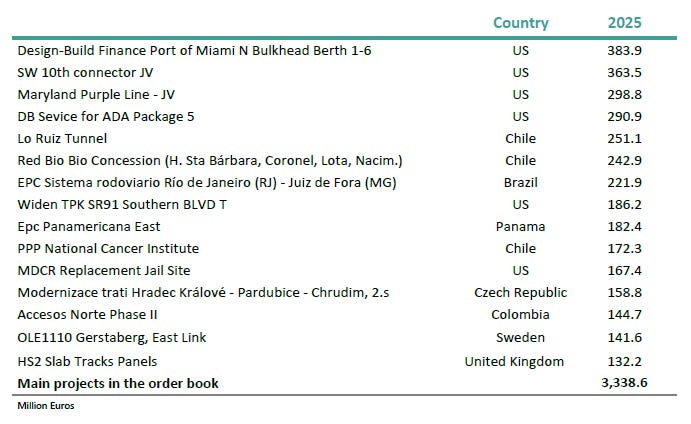

The construction order book stands at €7.904B, accouting for 28.7 months of sales. By geography, the US is the main region with 40.1%, closely followed by Europe 37.8% and Latin America 22.1%. By project type, the majority of the order book is concentrated on roads (30.7%) and railways (29.1%).

OHLA has made a successful effort to position itself in the US market with iconic projects like the Maryland Purple Line or the port of Miami expansion, taking advantage of the infrastructure investment boom required to update their aging public infrastructure.

Industrial (€116.3m Revenue, 2.89% of total Revenue)

This division focuses on industrial engineering, particularly complete industrial plants and systems, including the design, construction, maintenance and operation of oil and gas plants, renewable energy projects, etc.

Historically, it was positioned as a major growth vector alongside core construction. However, the division has shrunk significantly over the 2025 financial year (-59.8% vs 2024), acting as a drag on the group's performance due to a legacy mining project in Chile (more on that later) . In terms of profitability, the Industrial division experienced a challenging period in 2025, swinging to a negative EBITDA of -€18.8m (-16.2% margin) compared to a positive profit in 2024 (€11.5m, 4.0% margin). The revenue slump continued in Q1 2026 (€32.9m, -24.5% vs Q1 2025) but recorded strong profitability (€2.2m EBITDA, 6.7% margin) showing that the division is stabilizing. Also the order book has grown strongly in the past year to €201.6m (+34.9% vs 2024) which also points toward the fact that the worst is over.

Looking forward, management is steering the division toward lower-risk, turnkey contracts in core geographies like Spain and Latin America, aiming to stabilize the unit into a small, lean partner that complements the high-margin construction and concession engine without exposing the group to volatile industrial risks.

Concession Development

The Concession division is in charge of developing greenfield (newly created) projects, participating with concession groups and infrastructure investors in the study, development, financing and operation of projects.

The importance of the Concession business is not just on the future cash flows it will receive, but in the fact that it works as a feed for high-margin projects for the Construction division. Once OHLA Concessions is awarded a project, it directly awards the construction contract internally to the Construction division, generating immediate operational cash flows at a much higher margin because they don’t have to underbid other rivals.

Once the construction is complete, OHLA has the option to sell those concessions to pension funds or to infrastructure funds instead of keeping them until maturity. These institutional investors are hungry for these kind of assets due to the fact that they are completely de-risked, inflation-protected and carry highly predictable future cash-flows.

Geographically, most concessions are located in Spain and South America (mainly Chile). The revenue for this division is quite small and it’s not broken out as an independent major division. Instead, they are aggregated under the “Other” segment which includes minor corporate holdings and asset lines. The order book is just over a billion euros (€1.009B) highlighting the importance of the division for the stability of the group.

Developments

The smallest division of the company, it develops luxury real estate projects in iconic locations like the Raffles Hotel at the Old War Office in London (sold in 2021) or the Mayakoba City complex in the Riviera Maya in Mexico (sold in 2018). Not being in the business of managing luxury properties, OHLA usually sells the properties once the projects are finished.

Nowadays the division just encompasses the Centro Canalejas complex in the center of Madrid, a luxury development on a cluster of 19th century historic buildings which include the first Four Seasons Hotel in Spain, 22 Four Seasons-branded residences, a luxury mall (Galería Canalejas) and a 400-space underground parking garage.

The construction of the complex started in 2013 and was finalized in 2020 with the opening of the Four Seasons Hotel and Residences. Afterwards the mall was inaugurated, starting with the foodhall in the basement level in 2021 and then followed by the ground floor with luxury boutiques in 2022.

OHLA sold a 50% stake on the project on February 2017 for €225m to Mohari Hospitality, a global investment platform with a focus on luxury hospitality investments owned by Mark Scheinberg, the founder of PokerStars. Just a few weeks ago, OHLA and Mohari have decided to split the Centro Canalejas complex assets, making a possible sale of those assets by OHLA far more likely.

The whole Centro Canalejas complex reached 91.4m in revenue in 2024 (+29% vs 2023) and EBITDA more than doubled to 28.4m (vs 13.1m in 2023). Although this division is very small in terms of revenue and EBITDA, the uniqueness of the Centro Canalejas complex makes it a very valuable asset still in its early expansion phase.

Services (€566.5m, 14.09% of total Revenue)

Under its subsidiary Ingesan, OHLA is specialized in facilities management, mainly in the areas of:

Urban services - waste management, street cleaning, maintenance of parks, etc.

People Care services - management of nursing homes, depencency care, home care service, etc.

Cleaning - health centers, airports, government buildings, etc

Maintenance and Energy Efficiency - hospitals, government buildings, street lighting, etc

The vast majority of Ingesan activity is carried out in Spain with a small presence in Chile and Mexico. In 2025 the division reached €566.5m in revenue and €14.1m in EBITDA (vs €520.1m and €10.5m EBITDA in 2024), with a strong order backlog of €620.5m. While revenue is increasing at a decent rate (+11.6%), EBITDA disappointed falling well below management expectations of €18m.

The Services division is classified as held for sale so it could be sold at anytime as this kind of asset is highly valued by the market.

Clearing the Roadblocks

In the past decade the market has clearly penalized OHLA for having several obstacles ahead that the company had not resolved which could have impacted its economic viability. Lately management has made a great effort to finally remove this roadbloacks which included:

1 - Debt

The debt burden of OHLA has been a recurring headache for the company since the mid-2010s. Leverage reached more than 11x (GFD/EBITDA) in 2020 when the Amodio family landed on the company, making debt reduction their number one priority.

In October 2024, OHLA launched a capital increase of €150m at a price of 0.25€ per share to facilitate the refinancing of the company’s debt, which was close to €550m back then between bonds and bank debt. The Amodio brothers contributed €26m, Mexican businessman Andrés Holzer added another €25m and Spanish businessman José Elías, the majority owner of renewable energy company Audax Renovables (AUX.MC), led the raise with €50m. The capital increase was concluded at the end of 2025 and the cash raised was used to reduce 140M of the bonds principal.

After the capital raise, on November 2024, OHLA reached an agreement with bondholders for its recapitalization plan. Different bond issues were unified and pushed back, with the repayment being due now on the 31st December 2029. The sucessful debt refinancing had a very costly price: a coupon of 9.5% until December 2026 which jumps to 11.25% in 2027 and to 14.05% in 2028.

Also, as a part of the agreement with bondholders, OHLA accepted that any proceeds from asset disposals would be used to repay the debt.

Thanks to both operations, total financial debt was reduced to €311m at the end of 2025, a 31% reduction versus the previous year. The debt burden is still very heavy and it’s affecting the bottom line, but now the situation is more manegeable.

2 - Legal disputes

Another dark cloud hanging over OHLA were the legal disputes from some legacy projects, which could have put the company under high financial stress.

Doha Metro (Qatar) - in 2016, Qatar Railways terminated a contract with a JV were OHLA had a 30% stake to build several major stations for the Doha metro. Qatar Railways claimed that the JV defaulted on deadlines and failed to meet performance target. The International Chamber of Commerce (ICC) ruled that Qatar Railways’ termination of the contract was illegal and breached contract conditions in late 2023, and that ruling was confirmed in the 2025 final settlement where the ICC ordered Qatar Railways to pay the JV a total of €315m including procedural costs. In the end, OHLA is going to receive €45m in total compensation.

Sidra Hospital (Qatar) - on December 2025, the ICC issued its final award on a dispute with the Qatar Foundation regarding the contract termination for the construction of the Sidra Hospital in Doha. Back in 2014, the Qatar Foundation terminated the contract and sued a JV of which OHLA had a 50% stake for more than €950m claiming substantial delays on the project. At first the ICC awarded the Qatar Foundation €24.3m on damages, but the amount was reduced on December of 2025 to just €0.9m. OHLA had provisioned €28m in its balance sheet regarding this dispute which was the most significant contingency the company had faced in the last decade.

Jamel Abdul Nasser Avenue Viaduct (Kuwait) - another dispute in the Middle East which ended up being quite costly for OHLA. In 2024, Kuwait executed guarantees amounting to €39.2m regarding the construction of the Jamel Abdul Nasser Viaduct against a JV where OHLA had a 50% stake. The JV sued Kuwait for €278m before the ICSID (International Centre for Settlement of Investment Disputes) but it was finally rejected on March 2026. As such, OHLA lost the €39.2m in bank guarantees executed by Kuwait.

Mantos Blancos Copper Mining Project (Chile) - the Santiago Court of Appeals ordered subsidiary OHL Industrial Chile to pay $21m to subcontractor Syncore Montajes on July 2025 for unpaid work and relatated damages on a sulfide processing plant at the Mantos Blancos Mine.

Biobio Hospital Network (Chile) - OHLA and the Chilean government reached an agreement regarding the construction of 4 hospitals in the Biobío region. The Chilean government had previously tried to cancel the contract claiming OHLA was behind schedule but under the final settlement reached on November 2025 OHLA was given until 2030 to finish the project (previously 2027). This agreement saved a €400m investment for OHLA.

In the end, the legal disputes outcomes have not been as bad as expected, not affecting the economic viability of the company, which at one time was in doubt as the cases were mounting and the future was really uncertain. In a worst-case scenario they could have taken a huge toll on the company or even push it into bankruptcy. All in all, the cash inflow from the Doha Metro helps to make balance for the bank guarantees lost in Kuwait, the cash outflow from the copper mine in Chile plus all the litigation costs incurred on the past years.

3 - Canalejas Complex Split

At the beginning of February 2026, OHLA reached an agreement with Mohari Hospitality to terminate their Centro Canalejas JV and to split the assets at 50%. OHLA will keep the Galeria Canalejas mall and the majority of the underground parking garage (around 320 parking spaces), along with an associated debt of €45m. Mohari Hospitality will keep the Four Seasons Hotel and Residences, 80 parking spaces for hotel guests and the Hermés boutique (which was outside the Galeria Canalejas mall), along with €100m of debt.

This split paves the way for a potential sale of its assets on the complex on its own terms. There had been unsuccessful attempts to sell the whole Canalejas Project for €850-€900M (debt included); this asset split should make the asset sale easier for both parts if needed.

High Debt Burden Overshadows Improving Financials

Just a quick glance at the main financial indicators is enough to understand the turnaround OHLA has had in the last few years since the Amodio brothers took charge of the company.

In just six years, revenues have increased by 33%, EBITDA has more than tripled, leverage has been reduced from 11.3x to 1.7x and cash generation has gone from over €200m in cash burn to generating over €75m pear year (before investments and divestments).

As we have seen, the debt reduction and restructuring have helped a lot to improve its leverage, but it’s also true that and operating level the turnaround has been as impressive. As of early 2026 OHLA gross financial debt is at €362.4m, almost all of this is recourse debt while non-recourse debt (linked to specific projects) has been minimized.

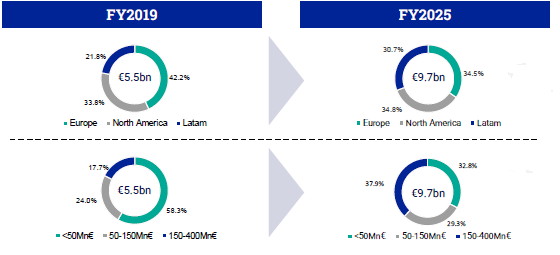

The turnaround is also reflected on the backlog, which has grown from €5.5B in 2019 to 9.7B at the end of 2025.

More importantly, the project size project size has also changed, with more projects in the €150m-€400m range compared to 2019 when most of the backlog were projects under €50m. By geography, LATAM has increased its weight thanks to projects in Chile, Mexico and Peru. By division, the bulk of the backlog comes from Construction (€7.9B), followed by Concessions (€1B) and Industrial (€201.6m). Book-to-Bill ratio remains at a strong 1.2x confirming high demand and high revenue visibility in the coming years.

The bad news is that the turnaround is not yet visible at the net income level due to the increase in financial expenses: the recent debt recapitalization meant a higher coupon and almost €13m of financial expenses associated with the racapitalization were accounted in 2025. As such, in 2025 a €194m operating profit translated to only €1.7m net profit (nonetheless an improvement vs a €50m net loss in 2024).

The good news is that OHLA has two assets ready to sell which can wipe out the totality of its debt boosting the bottom line almost instantly.

Assets Held for Sale

Galería Canalejas and Parking Garage

Clearly the most valuable asset of OHLA: the whole Canalejas complex generated €91m in revenue in 2024 and €28m in EBITDA (last accounts available). After the asset split, OHLA will keep the Galería Canalejas mall (€12.7m revenue in 2024) and the underground parking garage (€1.3m revenue).

OHLA management has clearly estated that the goal is to sell the asset, as they are not in the business of managing this kind of property. There’s no rush and they will take the time for the right offer to arrive.

Galaría Canalejas is clearly a trophy asset: an iconic historic building in the center of Madrid with the largest luxury houses of the world as tennants. Not only that, but Galería Canalejas enjoys tailwinds which can help to increase its financial performance and valuation:

Madrid Luxury Tourism Boom - Madrid has always been a laggard compared to its European counterparts, but lately luxury tourism is booming: tourists are attracted by its world-class cultural offer (museums, concerts, sporting events, etc) and gastronomy (3rd city in Europe with the most Michelin-starred restaurants), great weather and beneficial tax treatment of luxury shopping. All of this at a fraction of the price of Paris or London.

The Centro Canalejas Effect - after the opening of the Canalejas Complex, luxury hotel chains hurried to open nearby: a JW Marriott hotel was inaugurated 2 years ago and new luxury hotels in the area are expected to open soon (Bulgari Hotels, Nobu Hotel, Radisson Collection,etc) . The fact that LVMH-owned Bulgari Hotels is planning to open a new hotel in the area is the definitive signal that the area is consolidated. These new hotels are just in a 2 minute walk radius of Galeria Canalejas, which would bring more UHNW individuals to the area.

Room to Grow - Galeria Canalejas mall generated 120m in sales in 2024 (20% increase vs 2023) but the real highlight is that there was a 36% jump in boutique sales. That’s with an occupancy rate of just 69%. Galeria Canalejas is still in the early stages of growth, so 100% maturation will take some years to reach, towards the end of this decade.

The Basement Level Opportunity - the foodhall in the basement level has been the only dark spot in Galería Canalejas, as several restaurants have closed down due to poor sales. It was a risky bet since the beginning because the nature of the food hall business (low ticket and high footfall) clashed with the one of the luxury boutiques (high ticket and low footfall), which perform better the less people there are. Far from being a disaster, this can be an opportunity to match the basement level to the offer upstairs. Recently OHLA refinanced the Galería Canalejas debt adding a €9m capex facility to turn the lower floor into a luxury wellness and beauty spa by Aire Ancient Baths. That would be a great first step; after all it’s much more consistent with the Galería offer to sell €500 spa treatments than €15 tapas.

The Underground Parking Garage - an overlooked asset, the parking garage can be extremely profitable: zoning laws don’t allow for new parking garages in the center of Madrid, so many of the new luxury hotels opening in the area will have to rely on it. On top of that, the parking garage allows for increased security and discretion for VIPs who want to shop at the Galería.

Unique Asset - all in all, Galería Canalejas is a unique asset that cannot be replicated. Its heritage, location and the quality of its tennants make it an extremely valuable asset for the right owner. It does make sense that OHLA sells it, as it has not experience managing luxury commercial real estate, which is more suited for specialized REITs or Sovereign Wealth Funds.

The valuation of Galería Canalejas is quite difficult to tell due to the uniqueness of the asset as there are no comparables. Recently the Brenninkmeijer family (one of the richest european families who are the owners of retailer C&A) acquired the San Miguel Market, an early 20th century historic market in the center of Madrid turned into an upscale foodhall, for €200m, in which could be viewed as a similar asset as Galería Canalejas. It was previously acquired for €70m in 2017 so the asset has almost tripled in value in less than a decade.

This transaction proves that there’s of institutional hunger for central Madrid trophy assets. The Mercado de San Miguel is a mature asset that generates €10m in revenue vs €12.7m for Galería Canalejas which is still in its early expansion phase, so it demands a higher multiple. I think that OHLA could sell Galería Canalejas conservately for around €250m (plus debt) implying a 4% cap rate due to the quality of the asset and its growth profile.

I wouldn’t rule out if they keep the parking garage (a forever asset with almost zero maintenance costs) if they can wipe out enough debt by selling the mall. Also many potential buyers of the mall are not that keen in managing an underground parking garage.

Services Division (Ingesan)

The second asset held for sale could be the first one to go. Two years ago OHLA turned down a €60m offer by Serveo (owned by private equity firm Portobello Capital) for the Services division considering the price too low. Recently OHLA has relaunched the sale with a much better financial health: €566.5m revenue in 2025, €14.1m EBITDA and a strong backlog of €620m (increased to €641.6m as of Q1 2026).

Looking at peers, Spanish service company Urbaser was sold at 9x EBITDA to private equity firms Blackstone and EQT (€5.8B Enterprise Value and €650M estimated EBITDA) at the beginning of this year. Applying a much more conservative and achievable 7x multiple we would arrive at around €100m, which is the reported price tag that OHLA management has put on it

In total, I think that OHLA can get at least €350m from both assets, enabling the company to wipe out all its debt burden. The math is clear: in case of a sale of both assets, OHLA would lose around €14m in EBITDA coming from Ingesan and another €14m in revenue from Canalejas (which goes almost entirely to EBITDA); on the other hand, it would save around €40m on interest expense.

Let’s not forget that under the terms of the February 2026 agreement with bondholders, 100% of the proceeds from the sale of assets must go directly to repaying the 2029 bonds. That means that there’s no risk of management squandering the money.

Once the equity issue the ohla is not in a hurry to sell these assets, but the escalation of the coupon does mean that the sooner the better: at the end of 2026 the first coupon jump takes place, so it does make sense to divest these assets before that date.

2025-2029 Strategic Plan

Looking into the future, OHLA unveiled an ambitious Strategic Plan for the 2025-2029 period, targeting sales of at least €5B (+20% vs 2024) in 2029 with €300m in EBITDA (+111%), 6% EBITDA margin (vs 3.9%), and cash generation to double.

The strategic line of action for each of the division is as follows:

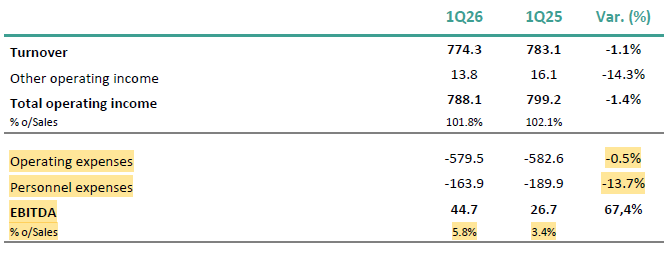

Construction - it will continue to be the main division of the company (approximately 85% of sales) focused on its core regions: North America, Spain, Czech Republic, Chile and Peru. The aim is to look for higher value-added segments with margins of at least 8%. One example is the recently awarded contract in Málaga (Spain) to build a microelectronics R&D centre. The growth will come mostly from the US, where sales are expected to rise over 80% in the period. The Q1 2026 EBITDA margin jump to 6.3% from 4.4% is a sign that the strategic plan is in the right direction.

Industrial - management has decided for the structural down-sizing of the division, deliberately exiting high-risk, volatile segments like Oil & Gas and complicated overseas industrial builds. The division will focus on standard, high-demand installations related to the energy transition (networks or storage) in core markets. The drop in revenue and the increase in EBITDA margin recorded in 2025 show that the strategy is working.

Concessions - it will focus on roads, hospitals and to a lesser extent railway projects, which are usually more complex. Geographically the aim is to grow in the US, Latin America and Central Europe. The division is designed to be the financial result generator for the group, directly contributing 8% of EBITDA by 2029.

Developments - management has clearly estated that they will look for smaller projects, as large projects like Canalejas “give more prestige than profits”. Following this new ethos, OHLA has started the development of a luxury residential project in the Spanish Mediterranean coast.

Services - back in 2024, the objective of management for the division was to discontinue operations in some geographic areas and activities which were no longer profitable. The increase in EBITDA in 2025 to €14.1m from 10.5m in 2024 shows that the strategy is starting to gain traction. The better the performance of the division, the higher its valuation regarding a potential divestment.

On the cost side, the aim is to streamline the organizational structure to seek greater efficiency and effectiveness as well as strengthen critical capabilities. The efficiency improvement plan is based on three pillars:

Simplify the structure of the Construction division to facilitate agility in decision making and standardization of reporting and control of operations. These initiatives could result in a reduction of about 7% in structural costs and 3% in indirect of costs.

Rationalize the organization of the Services division, merging business support functions and ceasing decitiary activities.

Strengthen the management model, including project control optimization of project purchases and improvement of operational excellence.

It is estimated that this plan could reduce costs by €40m, consolidating a decrease in structural costs over sales by 1% compared to 2024. The improvement in EBITDA is expeceted to be mainly supported by cost reduction and margin improvement until 2026, then revenue growth until 2029. Management wants to build first a leaner, more profitable company and grow from that base.

Q1 2026 results confirm that the cost reduction part of the plan is on the right path: despite lower revenue, EBITDA is already very close to the 6% target thanks to a large decrease in personnel expenses (excluding the Services division as it is accounted as an asset held for sale). From now on the focus will be on growing the top line while maintaining margins.

Stock Performance

If we look at the long-term performance of OHLA on the stock market, we realize how hard the fall has been. The company benefited from a construction boom in the 2000s until the 2008 GFC and it was able to bounce back from that low crossing the €30 mark again in 2014. But it was not able to recover from the second crash started in 2014: the stock lost 90% of its value in just a couple of years and it now trades 98% below that 2014 high.

In a shorter 3-year time period we can see more clearly the ups and downs in recent years: the stock is trading between €0.27 and €0.53, testing the top of the range several times but unable to break it.

The stock market is completely unaware of the transformation achieved this last three years: legal disputes have been solved, leverage is under control, margins are improving, EBITDA has tripled and cash generation is positive after a long time. Right now the market gives us the possibility to buy at the same price as 3 years ago when the company was in a far worse condition.

This buying opportinuty is also thanks to some of the main backers of the last capital raise: once the lock-up period is over, some insiders like José Elías are selling part of their holdings. From their perspective it’s quite understandable: the stock has doubled in less than 1.5 years and they have no chance of disputing control of the company to the Amodio brothers.

From a technical level, consolidating above the 0.50€ resistance level is the first target; from there the stock could keep climbing reflecting the improvement in fundamentals. If it’s unable to break 0.50€ soon, it would be very likely for the stock to go back to the €0.35-€0.40 level, offering a more conservative entry point in the middle of the range.

Valuation

OHLA stock is currenty trading at €0.474 per share (closing price on June 18th 2026), implying a Market Capitalization of €654.19m and a Total Enterprise Value of 908.19m (254m Net Debt as of end Q1 2026)

As I always like to point out, I don’t feel comfortable using a DCF method due to the many assumptions you have to make in several parameters (cash flow growth, discount rates, terminal value, etc) which are almost impossible to foresee several years into the future.

On top of that, the current situation of OHLA makes it nearly impossible to have any sense of accuracy: interest payments are eating up most of the operating income and a potential sale of non-core assets would drastically change the picture almost of overnight. Also because of its size, the company is not followed by many analysts so estimates are not very reliable.

EV/EBITDA Ratio Valuation

Using an EV/EBITDA ratio valuation, which is I think it’s the proper one to value OHLA, we arrive at the conclusion that is clearly undervalued against its peers. I am going to assume a 7% EBITDA increase in the coming years (both from revenue growth and margin improvement), which is more conservative than the 10% growth management guides for in the strategic plan to achieve the 2029 €300m EBITDA goal.

FY 2025 EBITDA - €208.1m —> 2025 EV/EBITDA = 908.19/208.1 = 4.36x

FY 2026e EBITDA - €222.78m —> 2025 EV/EBITDA = 908.19/222.78 = 4.07x

FY 2029e EBITDA - €300m —> 2025 EV/EBITDA = 908.19/300 = 3.32x

OHLA is trading just above 4x while european peers are trading on the 7.0x-9.0x. Applying a midpoint 8.0x multiple to 2026 expected EBITDA, we get to a target share price of €1.083 (128% upside potential vs last closing price).

The multiple discount could have been justified because of the legal battles and debt profile that OHLA had, but once those are cleared, the multiple should go back in line with peers sonner rather than later.

In the best case scenario that management is able to deliver on its €300m EBITDA guidance for 2029, we would be talking about an absolute bargain: applying the same 8x EV/EBITDA would get us to a target price of €1.52 per share (+220%). If the multiple grows further to the 10x-12x range, the valuation would skyrocket making a 5x return possible.

Potential Catalysts and Risks.

In order to close that multiple gap against its peers, there are some potential catalysts ahead in the near future for OHLA which could speed up the proccess. Also let’s not forget about the risks that the company could face if things don’t go according to plan.

Catalysts

Ingesan/Canalejas divestment - the most obvious and the most powerful catalyst, a sale of one of these assets will dramatically change the way OHLA is perceived by the market, mainly due the reduction in debt but also because management would show that OHLA assets are valuable.

Debt Restructuring - another clear catalyst would be a debt restructing resulting in lower interest expense. If OHLA can lower its cost of debt to the 6-7% range, that would be a massive improvment on top of the principal debt reduction.

Credit Rating Improvement - right now OHLA has a B- rating by Fitch and a B3 from Moodys (up from Caa2). Its risk profile limits the potential investment rom large institutional investors, which are usually restricted to invest on stocks with speculative grade debt profiles. Any improvements in credit ratings (which should happen due to lower debt, lower interest expense or both) towards the investment grade would welcome new invsetors with deep pockets.

Dividend Initiation - in the last earnings call, CEO Luis Amodio estated that OHLA could issue a dividend in 2027.

Index Inclusion - OHLA is part of the third-tier IBEX Small Cap index in Spain and it is not present in the Stoxx Europe 600 Construction & Materials. As the financial situation of the company improves, a jump to the IBEX Mid Cap index and inclusion in the sectorial Stoxx 600 index seems certain, which would bring instutional investors.

These catalysts are all of them interconnected and should happen one after the other once the first domino falls, creating a chain reaction: a sale of Ingesan or Canalejas would reduce the debt burden and pave the way for a debt restructuring in better terms (credit rating improvement should follow). Once the debt situation is under control, a lower interest expense would free cash flow to pay for dividends. Index inclusion should happen along the way of these events and the valuation multiple gap should gradually close.

Risks

No asset divestment before the end of the year - a clear risk is that OHLA is unable to sell Ingesan or Canalejas before the end of this year. Two bad outcomes would come from that: first of all, the jump on interest expense would hurt the results in 2027; secondly, it will mean that those assets are not as valuable as management thinks, making a complete turnaround of the company much more difficult.

Legal Disputes - more legal disputes could emerge because of delays, overcosts, etc which are common in the sector and could turn into a big headache if not addressed properly.

Inflation and Interest Rates - a sudden raise on inflation and interest rates could have a double impact on OHLA: firstly, the cost of raw materials and labor would increase affecting profitability; secondly, refinancing costs would jump higher if OHLA decides to refinance its debt.

Conclusion

OHLA has gone through a transformation in the last five years which has completely changed the company operationally while the market has not realized yet. Legal disputes are over, margins are improving, debt is under control but the company is trading on the same price range as 3 years ago.

The potential divestment of two non-core assets can radically speed up this turnaround, sending a clear signal to the market that a new OHLA has emerged and forcing the stock to double just to catch up to the valuation of its peers.